Mexico’s Mining Boom: What International Technology Suppliers Need to Know in 2025

From Colonial Roots to Modern Hubs: Mexico’s Evolving Mining Role

As global demand for critical minerals surges, Mexico stands out as a powerhouse—ranked as the world’s top silver producer and a key player in copper, gold, and fluorite. Its mining legacy stretches back centuries, rooted deeply in the cultural and economic practices of pre-Hispanic civilizations. Today, the country continues to play a vital role in international supply chains.While in recent years, the mining industry has faced headwinds under former President Andrés Manuel López Obrador, who opted for tighter regulations, a freeze on exploration concessions, andto nationalize lithium, Mexico’s mining sector is growing again and giving new opportunities thanks to the political change with new president Claudia Sheinbaum. As a trained energy engineer and former Environment Minister, Sheinbaum has brought a more pragmatic, science-based approach to governance. While the moratorium on new concessions remains, Sheinbaum’s administration is fostering open dialogue with industry, modernization of permitting procedures, and a clearer path toward sustainability. Combined with Mexico’s integration into the USMCA trade agreement, its rich geological portfolio, and a growing need for advanced technology and services, these signals suggest that Mexico is not only reaffirming its status as a strategic mining hub but also opening fresh opportunities for international suppliers of equipment, automation, and sustainable solutions.

This article explores how Mexico’s political reset, economic ambitions, and evolving regulatory environment are shaping a new era of mining—and what global companies can do to tap into one of the most promising markets in the sector.

Inauguration of Claudia Sheinbaum as 66th president of Mexico

https://apnews.com/article/mexico-president-claudia-sheinbaum-7d3599b39a7298df46e7eda34d80afee

Mexico’s Mineral Wealth: A Global Mining Powerhouse

Given the shifting political landscape, it’s important to ground this transformation in economic reality. Mining has long been a cornerstone of Mexico’s development—its legacy stretches back nearly 500 years. As of late 2024, the sector contributes 2.05% to national GDP and a substantial 8.6% to the industrial GDP, according to the Secretaría de Economía (Ministry of Economy).The industry generates more than 400,000 direct jobs within mining operations themselves and over 2.5 million indirect jobs in supporting industries such as logistics, equipment supply, and services. This broad employment base makes mining one of Mexico’s most significant economic engines. With over 1,200 active mining projects at different stages—from exploration to production—the sector continues to underpin regional economies and national export revenues.

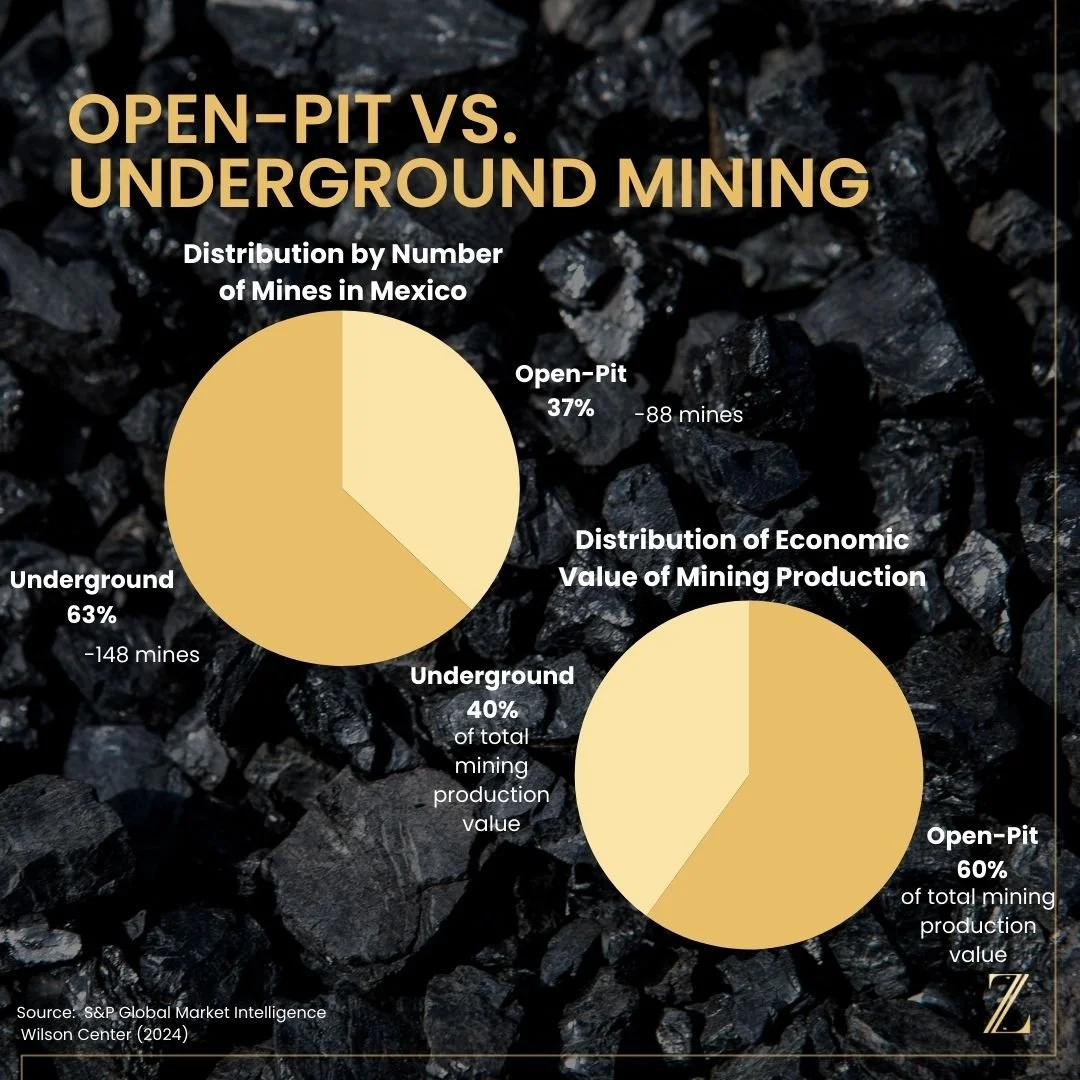

Mexico’s mining sector is extensive and internationally oriented. The country currently has close to 1,200 mining projects, of which 263 are already in production, spanning a broad range of metals and industrial minerals. Foreign investment plays a decisive role, with over 70% of all mining concessions held by international companies.

Mining exports contribute significantly to Mexico’s trade balance, generating more than USD 20 billion annually, primarily through the production of silver, gold, copper, and zinc destined for global markets. On the international stage, Mexico ranks among the top 10 producers of 17 different minerals, maintaining its position as the world’s leading silver producer for more than 13 consecutive years. This consistent output underscores the country’s importance as a strategic supplier of key resources to global industries.

While mining activities are present in nearly every state, a handful of regions concentrate the majority of production, exploration spending, and supplier networks, making them the key focus areas for foreign investment and service providers:

Sonora – Mexico’s top copper producer, driven by large-scale operations like Buenavista del Cobre. The state is also a significant gold producer and is becoming the center of lithium exploration, with projects such as Bacanora Lithium positioning Sonora as a future player in the EV battery supply chain.

Zacatecas – Known as the world’s silver capital, hosting major polymetallic mines like Fresnillo and Peñasquito. The state also produces zinc, lead, and gold, and benefits from an established mining services cluster and logistics links to northern Mexico and the U.S. border.

Durango – Rich in silver and gold deposits with a strong presence of underground mining operations, making it a hub for specialized mining equipment and safety solutions.

Guerrero – A key gold-producing region hosting major projects like El Limón-Guajes and Media Luna. Its well-known Gold Belt continues to offer strong exploration potential.

Chihuahua – A diversified mining region with a long tradition in silver, gold, and base metals. Its established mining ecosystem supports a strong network of suppliers and contractors, providing opportunities for foreign technology providers.

San Luis Potosí & Coahuila – Key centers for fluorite, zinc, and industrial minerals, vital for chemical industries and steelmaking. These states also have lower exploration risk due to long-standing operations and well-developed transport links.

The USMCA (United States-Mexico-Canada Agreement) provides additional strength to Mexico’s mining sector by guaranteeing tariff-free access to the key markets of North America. Minerals and metals extracted and processed in Mexico qualify as "originating goods" under USMCA rules, meaning they can be exported to the United States and Canada without facing tariffs or trade barriers. Especially in times of global uncertainty, this preferential treatment offers companies and investors stable conditions and facilitates seamless cross-border trade in minerals and processed metals.

Inside Mexico’s Mining Sector: Key Mines, Trends, and Opportunities for Suppliers

Mexico’s mining sector offers vast potential—but opportunities are concentrated in a handful of key regions and driven by flagship operations. Understanding where production is growing, which companies are investing, and what equipment and services are in demand is essential to successfully enter or expand in the Mexican market.

This section moves from the macroeconomic context into a ground-level view of the sector, highlighting the largest active mines, emerging projects, and regional clusters that define Mexico’s mining landscape today.

Key mines and flagship projects:

Buenavista del Cobre (Sonora) – Operated by Grupo México, this is one of the world’s largest open-pit copper mines, with production exceeding 450,000 tonnes of copper annually and a pit depth of over 1000 meters. The site is undergoing expansion projects to boost capacity and add new concentrators, creating demand for heavy equipment, automation technology, and environmental solutions.

Fresnillo (Zacatecas) – The world’s largest primary silver mine, mainly an underground operation reaching depths of over 1,500 meters, complemented by smaller satellite open pits. It produces silver with gold, zinc, and lead byproducts, driving demand for advanced underground drilling and hauling solutions.

Peñasquito (Zacatecas) – A large-scale open-pit operation and one of Mexico’s top producers of gold, silver, zinc, and lead. The mine features a vast pit over 2 kilometers wide and hundreds of meters deep, requiring extensive mining fleets, high-capacity crushing and processing technologies, and advanced water recycling solutions.

El Limón-Guajes (Guerrero) – A major open-pit gold mine with multiple pits up to 400 meters deep, ranking among Mexico’s leading gold producers. Operations generate ongoing demand for blasting services, high-tonnage haulage equipment, and energy-efficient ore processing systems.

Media Luna (Guerrero) – An underground gold and copper project currently under development, with planned mining depths of more than 600 meters below surface. Expected to sustain Torex Gold’s production well into the next decade, it creates opportunities for cutting-edge underground mining technology, shaft sinking expertise, and advanced worker safety systems.

Bacanora Lithium (Sonora) – An open-pit lithium clay project positioned to make Sonora a key global supplier for EV battery materials. The planned ramp-up, involving shallow pits of up to 100 meters, will rely on specialized extraction equipment, high-efficiency processing technology, and sustainable water and tailings management solutions.

Other Notable Sites – Chihuahua, Durango, and San Luis Potosí host a range of mid-tier silver, gold, and industrial mineral operations. While smaller in scale than the mega-mines, these projects often rely heavily on third-party suppliers for drilling, maintenance, and engineering services, making them accessible entry points for foreign companies.

Mexico’s mining sector is not only vast but also in the midst of a structural shift that is opening new opportunities for international players. Global demand for critical minerals such as copper, lithium, and zinc continues to rise sharply, fueled by the clean energy transition, electric mobility, and advanced manufacturing. This creates a strategic opening for suppliers and service providers who can help operators boost output efficiently and sustainably.

At the same time, the industry is embracing technological upgrades to improve productivity, safety, and regulatory compliance. Automation, drone-based surveying, advanced data analytics, and predictive maintenance are no longer optional but increasingly essential. International companies offering these solutions can establish long-term partnerships with large operators seeking to modernize operations and secure a competitive edge.

Sustainability has become a central factor in investment decisions. Companies that deliver innovations in water and energy efficiency, CO₂ reduction, and responsible waste management are well positioned to benefit from growing access to green finance and sustainability-linked investments. This aligns closely with Mexico’s broader ambition to modernize its industrial base while meeting higher environmental and social standards.

These trends are reshaping supply chains and procurement strategies. Operators are seeking reliable partners for equipment, consumables, and specialized services while building local supplier networks near production hubs. Regions such as Sonora, Zacatecas, Durango, Guerrero, and Chihuahua offer strong logistics links, established industrial parks, and proximity to the U.S. border, creating natural entry points for international companies aiming to integrate into Mexico’s fast-evolving mining ecosystem.

Partnering for the Future: How to Enter Mexico’s Mining Market

Mexico is in the midst of redefining its role in the global mining industry. With a new administration signaling pragmatism, a world-class geological profile, and increasing alignment with international sustainability standards, the country offers a rare blend of opportunity and transformation. For international companies, the message is clear: the time to engage is now.

But success in this shifting environment requires more than capital—it demands strategy, insight, and credibility. At Zeitgeist Consulting, we help international players navigate complex political and regulatory transitions, build trust with local stakeholders, and design market entry or expansion strategies tailored to the Mexican context.

Whether you're looking to assess risks, develop a stakeholder strategy, or reposition your operations for long-term success, Zeitgeist is your partner in building resilient, future-proof investments.

Let’s shape the future of mining in Mexico together—responsibly and strategically.

References:

Identec Solutions (2025) Minería en México: situación actual. Available at: https://www.identecsolutions.com/es/news/miner%C3%ADa-en-m%C3%A9xico-actual (Accessed: 4 July 2025).

Reuters (2024) Mexican mining sector balks at plan to ban open-pit mines. 15 February. Available at: https://www.reuters.com/world/americas/mexican-mining-sector-balks-plan-ban-open-pit-mines-2024-02-15 (Accessed: 4 July 2025).

Gobierno de México (2025) Minería. Secretaría de Economía. Available at: https://www.gob.mx/se/acciones-y-programas/mineria (Accessed: 4 July 2025).

Chambers and Partners (2025) Mining 2025 – Mexico: Law and Practice. Available at: https://practiceguides.chambers.com/practice-guides/mining-2025/mexico (Accessed: 4 July 2025).

Brown, E. (2024) Better together: USMCA and North American critical minerals flows. Brookings. Available at: https://www.brookings.edu/articles/better-together-usmca-and-north-american-critical-minerals-flows (Accessed: 4 July 2025).

Climate Bonds Initiative (2024) Sustainable Debt: State of the Market – Mexico 2023. August. Available at: https://www.climatebonds.net/files/reports/Climate-Bonds_Sustainable-debt-state-of-the-market-Mexico-2023_EN_Aug-2024.pdf (Accessed: 4 July 2025).

Fraser Institute (2024) Annual Survey of Mining Companies 2024. Available at: https://www.fraserinstitute.org/sites/default/files/2025-07/annual-survey-of-mining-companies-2024.pdf (Accessed: 4 August 2025).

Southern Copper Corporation (2023) SEC S–K 1300 Technical Report Summary: Buenavista del Cobre. Available at: https://minedocs.com/22/Buenavista-TR-12312021.pdf (Accessed: 4 August 2025).

Intergovernmental Forum on Mining, Minerals, Metals and Sustainable Development (IGF) and International Institute for Sustainable Development (IISD) (2022) Mining Policy Framework Assessment: Mexico. Available at: https://www.iisd.org/system/files/2022-11/mexico-mining-policy-framework-assessment-en.pdf (Accessed: 4 August 2025).